💧 Cash Flow Explained

You already know how to record transactions and calculate profit.

But here’s the catch — a company can show a profit on paper and still go bankrupt in real life.

How? Because cash didn’t arrive on time.

Cash flow is about timing — when the money actually moves, not just what the records say.

🧭 What Is Cash Flow?

💡 Cash Flow = Money In – Money Out

It’s the rhythm of your business — like a heartbeat.

When money comes in faster than it goes out, your cash flow is positive.

When bills are due but clients haven’t paid yet, it’s negative — and stress begins.

🏪 Real Example: The Café Problem

Your café sells coffee worth $10 000 in April.

But most customers pay with cards — and your payment processor transfers money next month.

Meanwhile, rent, ingredients, and staff wages are due right now.

- April Revenue (earned): $10 000

- April Cash Received: $2 000

- April Expenses Paid: $7 000

✅ Income Statement → shows $3 000 profit.

❌ Cash Flow → you’re –$5 000 short until May.

That’s why so many businesses struggle — not because they’re unprofitable, but because cash is stuck in transit.

Profit on paper ≠ cash in hand — cash flow depends on timing of payments.

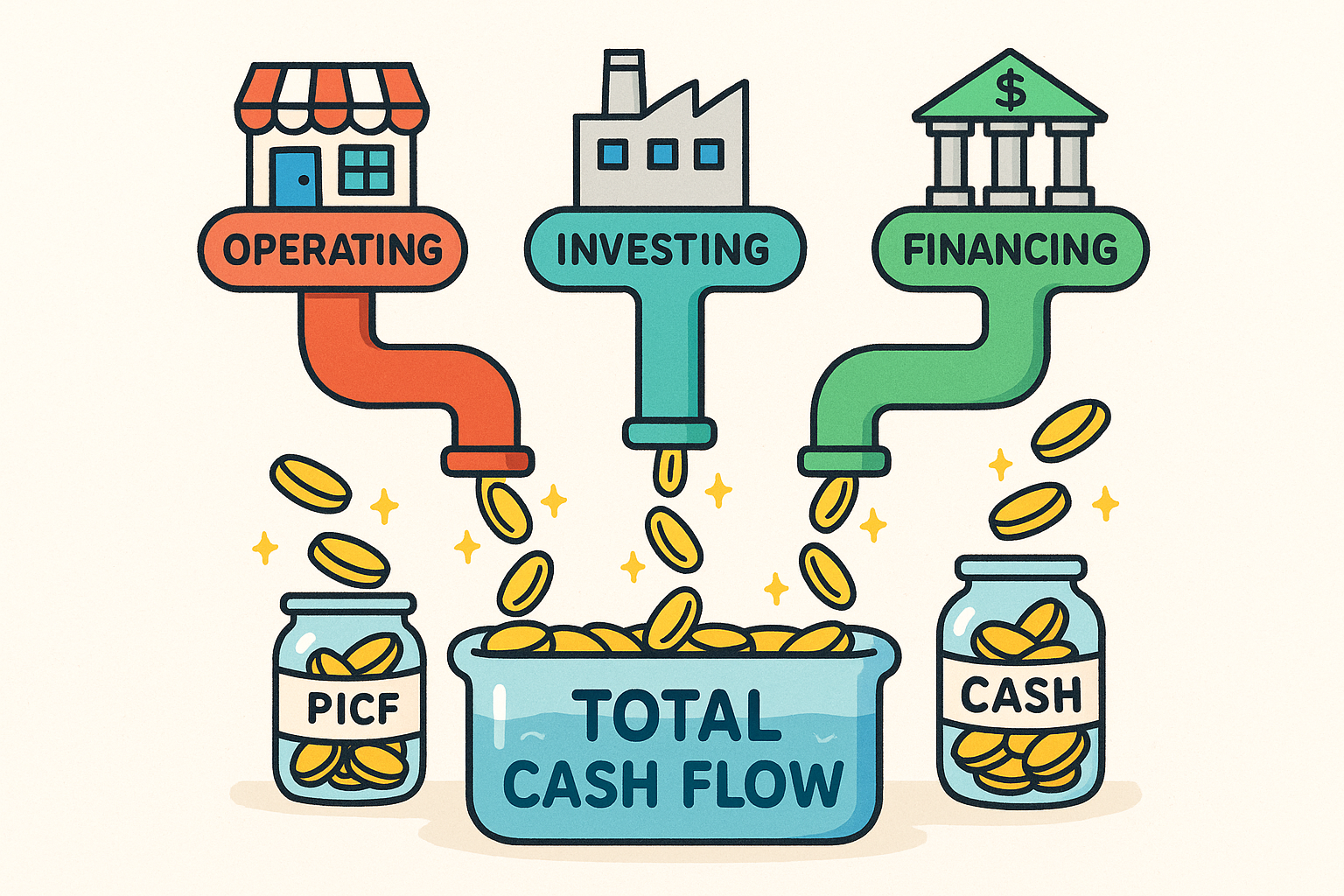

💰 The Three Types of Cash Flow

Accountants group money movements into three categories — they describe where the cash comes from and how it’s used.

| Type | Meaning | Examples |

|---|---|---|

| Operating | Daily income and expenses from core business | Sales revenue, salaries, supplier payments |

| Investing | Buying or selling long-term assets | Equipment, real estate, selling old machines |

| Financing | Borrowing or paying investors | Loans, repayments, issuing shares |

You can think of it as three pipes where money flows in and out.

The three cash flow streams — Operating, Investing, and Financing — combine to form the total cash flow of a business.

🧩 Cash Flow in Motion

Imagine your business as a tank of water:

- Sales bring water in.

- Expenses and investments drain it out.

- Loans add quick refills but must later be repaid.

As long as there’s enough water in the tank, you can survive dry months.

That’s why healthy cash flow means having cash at the right time, not just a big number at the end.

📊 Example: Sweet Days Bakery

| Category | Cash In ($) | Cash Out ($) | Net |

|---|---|---|---|

| Operating | 12 000 | 10 000 | +2 000 |

| Investing | 0 | 3 000 (new oven) | –3 000 |

| Financing | 2 000 (bank loan) | 0 | +2 000 |

| Total Cash Flow | +1 000 |

The bakery still gained $1 000 in cash overall, even though it bought an expensive oven.

That’s the power of understanding inflows and outflows separately.

🧠 How to Stay in Control

- Track timing. Know when each bill and payment happens.

- Keep a buffer. Always hold 1–2 months of expenses in reserve.

- Use forecasts. Predict future cash by looking at recurring patterns.

- Avoid illusions. Profit doesn’t mean cash — until it’s in your account.

💼 Try It Yourself

Track your own wallet or bank account for a week:

- Every inflow (income, gift, refund)

- Every outflow (food, transport, subscriptions)

Then sort them by type — operating, investing, financing.

You’ll start to see patterns in your personal cash flow!

Track your inflows and outflows — even a simple weekly view helps you make better money decisions and keep your cash balanced.

🌍 Real-World Application

Big companies rely on cash-flow statements every quarter to prove liquidity.

Banks look at them before lending money.

Investors study them to decide whether a company can grow without new loans.

Even small freelancers use cash-flow tracking to avoid missing rent while waiting for clients to pay invoices.

💬 Remember:

Profit shows success on paper.

Cash flow shows survival in real life.

In the next module, you’ll learn how to make decisions based on this data — turning numbers into business strategy.

📝 Try this today

Track every time money enters or leaves your wallet for 3 days.

Classify each movement as Operating, Investing, or Financing.

Complete the Accounting Mini-Exam to earn your Junior Accountant badge.

Lesson Progress

Module: accounting · +0% upon completion